ARTICLES

PUBLISHED ON LINKEDIN Data Governance’s New Frontier – ESG – Environment, Social, and Governance

By Malcolm Chisholm

It seems that the scope of Data Governance is ever-expanding and the complexity that the industry has to deal with increases every year. Recently, Data Privacy became vastly more important with the adoption of the EU’s General Data Protection Regulation (GDPR), the California Consumer Protection Act (CCPA), and many similar regulations in jurisdictions across the globe.

Now, something that is probably just as big and complex is on the horizon for Data Governance: ESG. Data Governance professionals need to know what this is, and how it is likely to affect them. Let’s take a look.

What is ESG?

ESG is an acronym for “Environment, Social and Governance.” It is primarily – at least today – focused on investing. That is, where investment decisions have to be made, consideration of ESG factors must be considered along with purely financial factors.

ESG is an acronym for “Environment, Social and Governance.” It is primarily – at least today – focused on investing. That is, where investment decisions have to be made, consideration of ESG factors must be considered along with purely financial factors.

The “environment” part tends to cover climate change, but also includes concerns such as biodiversity. “Social” aspects focus on how employees are treated and how minority or oppressed groups may be affected. “Governance” tends to be about corporate governance and ethical practices, such as anti-corruption and anti-bribery protocols.

Why is ESG important? Here are some reasons:

- The emerging reality seems to be that investments with good ESG credentials are going to have access to money with a lower cost of funding.

- There are many individuals and institutions that want to only invest in ESG activities. Fund managers who can attract this capital are going to be successful.

- Companies can promote themselves and enhance their reputation (and perhaps lower costs of access to funds and increase their stock prices) by proving they are compliant with ESG principles.

- Then there’s regulation. And in a repeat performance of Data Privacy, the EU is leading the way with ESG regulations – only it’s a lot more complex than Data Privacy.

Perhaps the easiest way to understand it is that more capital will be directed toward provable ESG activities, and these activities will be able to get investments at lower cost.

Greenwashing

As may easily be imagined, it would seem easy to simply claim compliance with ESG principles, if not outright lie about them, in order to gain some kind of advantage. A familiar example is a hotel (remember them?) with signage advising guests that by not laundering towels every day, the hotel is saving the planet. The real motive may be to reduce staff and laundering costs.

As may easily be imagined, it would seem easy to simply claim compliance with ESG principles, if not outright lie about them, in order to gain some kind of advantage. A familiar example is a hotel (remember them?) with signage advising guests that by not laundering towels every day, the hotel is saving the planet. The real motive may be to reduce staff and laundering costs.

While greenwashing is mainly thought of as simply deceptive advertising, it can be more complex. For instance, in the electricity market, “clean” states in the US may actually import “dirty” energy from other states. Complexity can increase even more with the way, say electricity, being categorized in environmental terms, with what is considered “renewable” and what is not, but these categorizations being goal-seeked to produce a more favorable ESG profile.

The EU Sustainable Finance Disclosure Regulation (SFDR) – and More

So how can greenwashing be stopped? And, in particular, how can ESG investors be assured that they really are investing in ESG activities? In the EU, the answer in part has been the Sustainable Finance Disclosure Regulation (SFDR). The SFDR is aimed a financial advisors and financial market participants, who have to comply with a number of measures, such as the integration of ESG risks into investment advice, and have policies about how ESG concerns are factored into their decision-making processes. The overall thrust is to have reliable ESG information for potential investors to consume.

But the SFDR cannot do all of this by itself. There are two other closely related initiatives: the EU Taxonomy; and the Regulatory Technical Standard (RTS).

The EU Taxonomy is a classification imposed on industrial sectors to identify which ones contribute to ESG. The basic industrial classification used in Europe, and on which the EU Taxonomy is imposed, is called NACE.

The RTS – of which a draft was published on February 2, 2021 – is where we get to see how all of this is going to impact Data Governance.

Trusted Data for ESG

Here are a few select points from the RTS concerning data:

- Polices used to evaluate principal adverse impacts (PAIs) must disclose the data sources used.

- Alignment to the Paris Agreement (on climate change) must specify “the methodology and data used to measure that adherence or alignment, including a description of the scope of coverage, data sources and how the methodology forecasts the future performance of investee companies.”

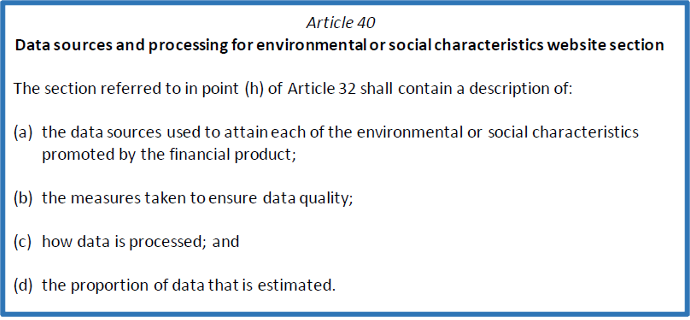

- Websites for financial products must disclose “Data sources and processing” and “Limitations to methodologies and data.”

And here is Article 40:

Here we can see familiar Data Governance concepts, and we can easily conclude that Data Governance is going to play a big role in making sure ESG metrics can be trusted. Admittedly, we are looking at a European perspective, but the framework that has been established is so detailed that it will be very tempting for other parts of the world to adopt large parts of it – albeit with some modification.

Many companies in the USA are already producing ESG metrics or thinking about it. The sooner Data Governance can be involved with these metrics, the better the outcome will be. The EU framework can provide a sound basis for what Data Governance should be doing. In any event, ESG is coming in a big way and all Data Governance professionals need to be prepared for it.